The following section is intended as an exploration of the history of money and housing and as a speculative exploration of the societal changes that could result from the widespread adoption of distributed ownership of real estate. For more detail on the short- to medium-term Groma roadmap, see our whitepaper.

In the year 2071

Mr. Yorage discusses the history of currency with his AP Macroeconomics class.

Good morning, class – I hope you all enjoyed your weekend. Can anyone remind us where we left off on Friday?

We’d just started into the history of currencies.

Yeah, and you were gonna tell us how to make loads of money!

Mr. Yorage

Thanks Francesca – and no, Frederick, I was talking about how governments over time have made lots of types of money… as in monetary systems.

Okay everyone, open your SophOS to our module on currencies. External network access is going off now, so finish up any chats please! Before we start with the new material for today’s lesson, let’s refresh a bit. You all use it every day, but could someone remind the class of the technical definition of GromaCoin we learned last week?

Francesca

One GromaCoin is equivalent to a tiny portion of the Gromabase.

Mr. Yorage

And what’s the Gromabase?

Frederick

Land! Tons of it.

Mr. Yorage

Let’s be a bit more specific please. Brett?

Brett

Well, it says here that it’s equivalent to roughly 15% of all residential and commercial real estate in the US, plus a harder-to-define percentage of the market in other countries.

Not just ‘equivalent to’ – that’s actually what it is, right?

2.1 Real Estate & Currency

Mr. Yorage

Yes, that’s it. One GromaCoin literally constitutes ownership of about one six-trillionth of the Gromabase. It’s an interesting place to start our lesson because it’s the largest and oldest realcoin foundation, but there are many other realcoins you’re probably familiar with as well.

And why are so many people willing to sell valuable goods and services that they can actually use, like sandwiches or hyper-simulacra, for GromaCoin, which are, in a literal sense, just some 1s and 0s on a server somewhere?

Brett

Because bricks grow more bricks!

Mr. Yorage

That’s not wrong, Brett, but how would you explain that if it were asked on a test?

Brett

Uh… ok. GromaCoin represent partial ownership in real estate assets, so each one produces dividends from those assets, and also the real estate value itself grows over time… so basically what I said, bricks can grow more bricks.

Mr. Yorage

So you did read the material – that’s pretty much right! But let’s take it one step further. Who can tell me why one might use real estate as the base for a currency? Certainly other things yield profits and increase in value over time, like shares in DisNetflix?

Ibn

That’s because real estate is a fundamental input to the economy, but entertainment isn’t.

Mr. Yorage

Right – although entertainment companies produce valuable products, most other sectors of the economy don’t rely on them as inputs for their own productivity in the same way that nearly every sector counts real estate among its inputs at some point. Even the most space-efficient tech companies still employ workers who have to live somewhere and servers that need physical racks some place. Any other reasons?

Mr. Yorage

What if there were a big scandal at DisNetflix that caused its stock price to drop 40% in a week?

2.2 Coupled Currencies

You mean like last year when they got sued when customers found out their holo-simulators were monitoring users’ REM sleep neural activity to target future content? Well, if the asset underlying your currency dropped 40% in a week, that would mean businesses would have to increase their prices really fast, which would be problematic in a few ways.

Plus, you said that uncertainty is bad for markets, so you would want something less volatile than stocks.

Yes, that’s right. Money tends to be most effective when it doesn’t vary wildly in terms of either supply or demand, and one way to achieve this is to tie money to something that has provable value and is thoroughly incorporated into the functioning of the economy. We call this “coupled currency”, because it’s correlated, or “coupled”, in both quantity and value to the commercial activity for which it’s used. This makes intuitive sense to most of us today, but it’s actually been a topic of much debate in the past and for many centuries was not how things worked.

For example, let’s imagine you run a sandwich shop, and I walk in and offer to pay you with a currency that’s based on nothing tangible, except that everyone currently agrees it’s worth something. How comfortable would you be giving me a sandwich for that?

Brett

Not very comfortable!

Ibn

A currency based on...nothing? What do you mean?

Francesca

Yeah, how can a currency be based on “nothing”? How is that even a currency?

What if I told you that almost all of you have used a currency based on nothing, and that not only is it the oldest currency in continuous use in the US, but that most currencies throughout history haven’t been based on anything with major practical relevance to the economy?

You’re talking about dollars, right?

If that’s the case, why do so many people use them?

Is that why they’re worth less every year?

Mr. Yorage

Yes, I’m talking about dollars. These are all great questions, and I promise I’ll get to them later in today’s lesson, but first we’re going to go wayyy back in time to the origins of money. Give me a second to set your SophOS to the right section...alright, let’s dive in!

2.3 Early Economies

SophOS

Self-Optimizing Pedagogical Help OS

Mr. Yorage

In the earliest economies, people who wanted things that they didn’t produce themselves would barter to get them. Two bushels of grain might be exchanged for a chicken; 100 square meters of cloth might be exchanged for a plow. While this worked, it had significant downsides. All of these goods are bulky and inconvenient to bring to every transaction, which led ancient civilizations all over the world to independently begin using scarce objects with primarily symbolic value — like cowrie shells or precious metals — to represent fixed amounts of each of these desirable goods. Not only did this solve the bulkiness problem, it also reduced the mental effort required. Instead of having to remember the exchange rate for every possible pair of goods, a market participant only had to remember each good’s value in, say, shekels, making the price system’s complexity scale only linearly rather than quadratically with the number of types of goods.

Explore SophOS

Pop Quiz

You live in a premodern society. As a single participant in the economy, you frequently need to barter for goods and services you can't produce yourself.

This is much more flexible. We only need two conversions to understand the value of a house in terms of apples. And remember, this advantage scales with the number of types of goods in the economy, which is likely to be much higher than the five shown here.

2.4 Early Currencies

It’s something we take for granted today, but for these early societies, the concept of money represented a genuine technological advancement — a process improvement that changed people’s lives for the better. The fact that currency was invented independently all over the ancient world by many different civilizations showcases the near-universal value of some form of currency exchange. Each currency took a different form but served a similar purpose.

Explore SophOS

Early societies used a variety of rare or symbolic materials for currency.

Many of these societies learned over time that it’s quite difficult for a currency with more symbolic than practical value to stand on its own. Yes, gold and silver had some practical uses, such as for jewelry and other forms of art, but it would be difficult for the average market participant, who had little use for these substances in their daily life, to come up with a valuation that would be shared by enough other market participants to be useful as a currency. Instead, rulers would decree that one unit of their currency was worth a specific amount of a staple commodity and let the markets figure out the rest from there. This was the system in ancient Babylon, in which each of the silver coins known as shekels was worth 160 grains of barley. In essence, this currency was backed less by silver than by wheat, which was a core input to the agrarian economy of the time.

2.5 Seigniorage

This kind of central coordination was useful, and potentially even necessary, in ancient environments that lacked the information distribution technologies, like the Internet or the printing press, that we enjoy today. By laying down a unifying standard, states streamlined commercial transactions for their subjects. Since the official value of a coin was generally higher than that of the metals it was made from (a phenomenon known as “seigniorage”), these states also secured an extra income stream for themselves. For instance, a silver coin worth 100 cents might only contain 90 cents worth of silver, so every coin generated would net ten cents for whichever ruler had the rights to mint it (a profit that would be realized when the coins were used by the government to purchase goods and services).

But since states, through their monopoly on the legitimate use of force, were able to prevent other entities from providing competing currencies, they eventually realized that they could manipulate the details of the currencies they controlled to their advantage. Changing the metallic composition of coins to a cheaper mix — say, from 90 cents worth of silver to 60 cents worth of silver and 5 cents worth of zinc — increased the rate of seigniorage, allowing rulers to transfer wealth from their subjects to themselves without attracting the same level of attention that a tax hike or a forcible seizure of assets might.

Since means of determining the composition of coins weren’t widely available in ancient times, rulers had a large degree of latitude in making these changes. But as the sciences advanced, and measurement tools became more common, it became easier to hold rulers to account by demanding pure currencies, with gold and silver being the most common.

While this was an improvement relative to the less-accountable systems it replaced, it ran into challenges of its own. In Europe, for example, the most common commodities used to back currencies were gold and silver. The use of these two metals as stable stores of value was predicated on the relatively predictable supply available to the Old World empires, but the discovery of the New World would upend this relationship. When Spain found tens of thousands of tons of silver in the Andes in the 16th century, it quickly became one of the richest empires in Europe, using its newly minted ‘pieces of eight’ to import goods from all over the world, and, unintentionally, creating significant inflation elsewhere in Europe by flooding the market with newly minted currency.

2.6 Promissory Notes

In the midst of these challenges stemming from the relationship between money and metal, another form of currency was gaining steam in Europe. Promissory notes, or legal documents specifying the terms of a debt to be paid, had long been traded between parties other than those for whom the document was originally written. For more context on how this might have worked, read this short story.

In this way, promissory notes served as a currency of sorts, though they were not standardized or used by broad swathes of the populace outside of money-trading circles. Scaled adaptation would require either a high degree of trust between users or a centralized, accepted authority to enforce the debts.

While this technique evolved independently in many regions, widespread usage occurred first in the 17th century in Europe, when public (i.e. government-run) banks began issuing large volumes of debt as paper money to finance the various projects of their respective states (largely war with each other and colonization elsewhere in the world). For example, if the English government needed to build a new fleet of warships to compete with France and Spain in the New World, it might issue a large amount of silver-backed paper money to pay the shipbuilders. Then the shipbuilders could spend this money on whatever else they needed to run their businesses or buy necessities for themselves.

As everyday people became more comfortable with treating specially marked paper as being equivalent in value to precious metals, the need for these notes to bear interest in order to be accepted declined. So instead of a note being a true debt instrument, i.e. offering the holder a stated value back plus interest over time, the notes evolved into something much more like the paper currency that dominated the 19th and 20th centuries, with a fixed value in nominal terms.

2.7 Fractional-Reserve Banking

Around the same time, private banks began to adopt a practice known as fractional-reserve banking, in which they transitioned from keeping 100% of their deposits available for withdrawal at any time by their customers to keeping only a much smaller amount of deposits in reserve (10% or so) and loaning the remainder out. This might sound risky (and to some degree it was; if everyone tried to withdraw at once it could cause the bank to become insolvent, i.e. unable to allow depositors to fully withdraw their money — a phenomenon known as a run on the bank), but experience demonstrated that, outside of rare occurrences, depositors tended to keep enough money in their accounts for banks to loan confidently within the constraints of a given reserve ratio. This financial innovation enabled the total value of loans/money banks issued to exceed their total reserves of cash by a significant multiple, thereby stimulating much more economic activity than had been possible previously. This allowed the countries best able to master it — England being the primary example — to take a decisive economic lead over their rivals.

So let’s review. Initially, currencies literally were assets, e.g. coins made of metal. Then, currencies became paper, which was redeemable for assets. Banks went through an analogous evolution. Initially, they held depositors’ assets; if you were a depositor, your deposit was your specific bar of gold or silver. Then, under fractional-reserve banking, your deposit represented a generic claim on assets of a specific value that would be drawn from whatever the bank had on hand at the time, allowing the bank to lend out the majority of its deposits.

Now let’s take a look at states, which went through a similar evolution. Initially, states issued metal currency or paper currency backed by hard assets, i.e. 1:1 backed by grain, silver, or gold. Then they realized they could stretch this ratio and issue much more currency, keeping only a fractional reserve of the backing asset. This new paper currency could be spent by the government and was functionally debt since it could theoretically be redeemed for the underlying asset upon request to the central bank. In this way, states functionally merged the processes of public debt issuance and new currency provision. States weren’t just overseeing the validity of paper currency to facilitate commerce and then taxing commerce to fund their operations; they were issuing wholly new money to fund their operations, which then also expanded the supply of money for taxable economic activity. SophOS can give you a more detailed history on the relationship between metal and money for those interested in bonus reading.

2.8 Full Currency Uncoupling

The last gasp of widespread asset-backed money emerged in the aftermath of World War II in the form of the Bretton Woods system. This system was the result of an agreement between the western Allied powers and Japan to set fixed exchange rates between each of their currencies and the US dollar, which would in turn be redeemable for gold at $35/oz with the US government. The goal was to ensure a reliable environment for international commerce, with stable rates of exchange and lowered potential for competitive devaluation. However, a combination of inflation, public debt, and a current account deficit in the US resulted in overvaluation of the dollar relative to other currencies, which led other countries to begin exchanging their dollar reserves for gold.

With gold reserves dwindling, on August 15, 1971, President Nixon ended the dollar’s convertibility with gold. This began a period dominated by pure fiat currency that would last for almost 70 years. Relative to earlier periods, this gave the federal government significantly more latitude to respond to economic downturns by increasing the money supply. A series of economic shocks were accompanied by massive fiscal stimulus and quantitative easing (QE) programs to get the economy growing again.

Explore SophOS

2008

A global financial crisis

$2 trillion

Each package was effective in driving growth, but also resulted in the functional printing of trillions of new dollars that naturally led to a decrease in the value of each dollar and, more damagingly, a decrease in confidence in the long-term value of the dollar. All of this drove up inflation, bit by bit, until the inflation rate peaked around 20% annually in the mid 2030s. The Meijer administration aimed to solve this problem with the Currency Stabilization Act of 2039, which succeeded in bringing inflation back to the single digits, but the damage to trust in the dollar and its status as the world’s reserve currency couldn’t be repaired so easily. Throughout the preceding three decades, increasing numbers of people had begun to recognize the risks associated with the dollar and to seek out stabler alternatives. Gold and silver were a part of this as always, but new entrants like cryptocurrencies and a variety of different types of decentralized money quickly jumped from experimental status into trillions of dollars of total market value.

Mr. Yorage

Now, before we talk more about the history and social impact of decentralized currency, which I’m sure you all know something about, what are some examples of decentralized currencies other than Groma?

Ibn

GigaJoule!

Linda

MooreCoin!

Frederick

Asclepius!

Mr. Yorage

Good. And what do all of those currencies have in common with Groma that earlier currencies didn’t?

Brett

They’re all connected in some way to things that people and companies all need to use often – energy, processing power, and healthcare, respectively.

Mr. Yorage

Exactly. Even the decoupled currencies that were backed by real assets, like gold-backed dollars or silver-backed pounds, didn’t have the same kind of direct connection to goods or services that the average person would use regularly. Of the three you mentioned, Asclepius is the most similar to Groma, since it confers partial ownership of a constant revenue stream — that of participating firms in the longevity industry – whereas GigaJoule and MooreCoin are directly tradable for pre-defined amounts of energy and processing power. This type of input-backed currency has become a mainstay of our economy over the last 30 years, but why? What advantage does it provide that other currencies can’t?

Mr. Yorage

Has anyone learned about the episodes of hyperinflation in Germany in the 1920s and in Venezuela in the 2010s and 2020s?

Clio

I read that people were bringing wheelbarrows full of paper money to the store in Germany.

Francesca

And didn’t lots of people in Venezuela stop using their national currency, instead relying on black market US dollars and Bitcoin?

Mr. Yorage

Yes, that’s right. When inflation gets high enough, people feel pressured to find alternate sources of value storage, and when they do have soft money in their wallets, they tend to prefer to spend that money as soon as possible, since they know it won’t buy them as much if they hold onto it. People rationally hoard vital goods, causing persistent shortages in supply. Saving and many other forms of long-term planning become essentially impossible, and much economic activity shifts to the black market, which tends to use the most stable currencies available. At the end of the day, people want to know that the money they earn today will still be valuable enough to buy them what they need a year, a month, or a day in the future, and high inflation makes that uncertain.

Things never got quite that bad in the US in the late 2030s, but people were worried they might. As a result, consumers started shifting towards currencies that they knew by definition would enable them to purchase the same predictable amounts of essential goods and services as when they first acquired them. People would cash most of their paycheck out into Ether, Groma, GigaJoule, Asclepius, gold, stocks, or durable purchases, keeping just what they needed in dollars to make short-term purchases from vendors that didn’t accept these other currencies yet. For more information on how the transition to coupled currency occurred, take a look at the Gromafied Economy.

2.9 Decentralized Currencies

Since most people elect to receive the majority of their paychecks in realcoins like Groma or Asclepius, which appreciate over time relative to general consumption, the money in their accounts actually increases in terms of real value. People don’t have to put as much effort into picking smart investments in the stock market because the currency itself is an effective investment. Savings rates have increased steadily alongside this trend since people trust that their currency stores will yield compounding returns down the road. And because each of these currencies is forced to compete with all of the realcoins in an open market, the same competition that keeps businesses performant keeps these currencies in relative balance. There is no legal tender mandate for any of them, so the operating boards have to compete with each other for consumer and business trust. This was true to some degree of the Federal Reserve of the US versus the European Central Bank of the Eurozone and the Central Bank of the Republic of China. Technically they competed, and still compete, with each other, but each could rely on hundreds of millions of captive users, which created a somewhat monopolistic monetary ecosystem in each country.

In addition to transforming the ways in which we use and think about money, each of these new currencies had a lasting impact on the actual industries on which they’re based. They all have unique, interesting stories, but for the sake of time, we’re just going to cover Groma today, and your homework assignment will be to read about the others and come up with a new hypothetical realcoin of your own to present to the class tomorrow.

Intercom

Sean, could you please send the Macintosh twins down to the office?

Mr. Yorage

Sure. Francesca, Frederick, go ahead. I’ll send you the lesson materials later today. Why doesn’t everyone else take a few minutes to stand up and stretch a bit and then we’ll transition into the second-order effects of realcoins.

3.1 Introduction to Housing Policy

Mr. Yorage

So — Groma is a realcoin, and we’ve talked about the coin part, which tends to be similar across all realcoins, but equally important is the real asset — energy, real estate, healthcare — on which they’re based. So let’s talk about the real part of Groma and how housing and land usage changed with a currency based on real estate as a shared and widely owned resource.

For much of recent history in the developed world, owning one’s home has not only been a symbol of social status and self-sufficiency, it has been a powerful practical tool for building a durable, reliable base of personal wealth. Owning the home in which you live removes the necessity to pay rent monthly to someone else and enables you to benefit from the appreciation of the underlying asset. It was therefore considered a wise step for those who could afford it. Additionally, homeownership was seen as promoting stable families and giving people more of a stake in their neighborhoods and in the physical upkeep of the home itself. But the leap from renting an apartment to making a down payment for a home was a significant barrier for both individuals and the existing banking system in the early 20th century. To this end, starting in the 1930s, the US federal government began heavily incentivizing homeownership by providing mortgage financing, mortgage insurance, and tax incentives for mortgage debt, making mortgages much more affordable; as a result, the portion of households that owned their own home increased from slightly over 40% to roughly two thirds by the turn of the 21st century. This high rate of owner-occupiers was therefore not just an expression of the natural preferences of the households involved, but also a function of major government intervention to support it.

But this approach to housing policy was not without drawbacks. A government-prompted loosening of lending standards in the first decade of the 21st century that aimed to continue increasing homeownership rates was one of the contributing factors behind the financial crisis of 2008. The US economy eventually recovered from that shock, but other drawbacks remained. On a fundamental level, although owners of a discrete home are incentivized to make improvements to the home itself, their incentives with regard to the status of the surrounding neighborhood tended to net out towards keeping the overall housing supply as low as possible. That was mostly good for current homeowners, but bad for everyone else.

Imagine you own a single-family home in a relatively quiet, less dense part of a large, economically dynamic city with lots of excess demand for housing. There’s a plan to build a big residential development in a vacant lot across the street that would allow hundreds of new people to move into the city, which would not only increase the income and quality of life of the new residents, but would also create significant positive spillover effects for all of the shops, restaurants, and other businesses in the city that would now have new customers. This would be a clear benefit for the developers, the potential new residents, and the existing businesses, but the neighbor across the street might have different priorities. Why might that be?

Their street would get busier and noisier?

The new building might block the sunlight from their house?

Mr. Yorage

Yes, and they’d experience a year of potentially annoying construction activity. All are likely reasons that the neighbor might not want the new development. Can you think of anything more abstract? Potentially related to what we covered in the first week of class?

Brett

We learned about supply and demand that week...so if the new development increases the supply of housing without changing the demand, that means the price of housing should go down. And that would make the neighbor’s home less valuable, right?

Mr. Yorage

That’s exactly right. Many homeowners believed — and there’s still some debate today over which side is correct on this — that increasing the local housing stock would reduce the value of most existing units, including their own, which gave them a strong incentive to fight against such growth. For many people, a majority of their personal wealth was locked up in their home — a relatively illiquid asset. It’s not as if they could easily move to a new home, like a renter might, so they had strong incentives to limit development and maintain the upward value of that home. Again, good for existing homeowners in a city, but unfortunate for those who would have moved into the city if new projects were approved. Because only current residents can vote, and their motivations skew towards limiting new supply, the processes governing new development evolved to be heavily biased towards inaction. Extreme stories like Bob Tillman’s multi-year saga of trying and being stopped from developing new housing in chronically supply-constrained San Francisco became the norm and contributed to ever-increasing homeownership and rental costs.

3.2 Concentrated Costs and Diffuse Benefits

To understand this situation better, we should examine the underlying economic principle that guided real estate development for most of the 20th century and the first half of the 21st – that of concentrated costs and diffuse benefits. If one group is heavily invested in the outcome of a particular policy issue — generally because they have a large financial interest in it or live in an area immediately impacted by it — their voting and lobbying efforts will often depend entirely on that issue. Most other people won’t care enough about the issue for it to influence their voting decisions, even if it affects them to some degree. This means that, even if the total benefit of approving new housing to the city (or country) as a whole outweighs the cost to its immediate neighbors, the benefit is spread so thinly that a given person in another neighborhood who wants the development won’t fight nearly as hard as the development’s neighbor who opposes it.

3.3 Multipolar Traps

Since this pattern applies to each neighborhood, it has the potential to fragment incentives, with everyone acting rationally on their own self-interest, making everyone in the city, country, or world worse off in the long run. Because of the reciprocal nature of this dynamic, it can be described as a multipolar trap: a type of coordination problem in which everyone would prefer a different overall outcome that could in theory be achieved if everyone cooperated, but each individual is incentivized to do what’s best for themself in the short term, so everyone is stuck with an undesirable general outcome.

For a long time, cities and the people within them lacked any kind of effective coordination mechanism to overcome this dynamic. That resulted in fewer homes being built than were needed and the cost of homes increasing far faster than overall economic growth consistently from 1920 through 2020. The cost of renting appreciated similarly, accelerating a transfer of wealth to the land-owning class.

That trend began to change with the introduction of Groma. Just as GigaJoule enabled consumers to express a strong preference for renewable energy sources and resulted in the Second Green Revolution slowing the pace of global warming, and the broad adoption of Asclepius increased average life spans over the last 50 years, the adoption of Groma created a fundamental shift in the real estate industry.

How did this occur? A few steps had to happen.

3.4 How Groma Changed Housing

Explore SophOS

- Groma made it easy to invest in real estate

Groma shrank the initial step towards real estate ownership from buying a whole home to buying a single GromaCoin. Incremental real estate ownership became generally accessible and opened up a parallel path to home ownership. Rather than owning a single home and living rent-free, many chose to own a “liquid home” in Groma and use the dividends to pay rent wherever they chose to live.

- As a result, people became more committed to improving neighborhoods far and wide

This more mobile population had different preferences, which led to the second major change. Instead of wealth being concentrated in a single piece of property in one neighborhood, it was spread thinly across many properties across many cities as Groma combined flexible renting with flexible ownership.

This changed how people thought about the real estate around them. Rather than just caring about their specific plot of land, individuals became interested in the improvement of their neighborhood and other neighborhoods where they might want to live in the future. Everything that improved land value improved their wealth and future living options.

- And began voting on real estate projects worldwide, thanks to Polis

The final change was a more advanced mechanism of projecting these preferences. Polis, which everyone has the right to participate in once they turn 16, is a system of distributed polls that enables larger populations to easily weigh in on projects, as opposed to just a small group of neighbors or those with the time to attend city council meetings. Polis counterbalanced the problem of concentrated costs and diffuse benefits with a system that slightly increased the value and awareness of those diffuse benefits and made it far easier for that diffuse population to have a coherent voice.

3.5 Polis

Mr. Yorage

So let’s talk a bit about the history of Polis. First, we should define our terms. The key terms here are Polis and Strata.

Ibn

Geoscalar Polling Core?

Mr. Yorage

Sorry, yes, what we often call Strata is actually an incorrect usage of the word. The real system is called a Geoscalar Polling Core. Can anyone tell me what the difference is between those two terms?

Polis

The system by which individuals are able to express their preferences on a given planned development in a city.

Strata

The concentric zones by which votes are grouped to provide panels of voting preferences organized by geographical relevance

Ibn

So a Stratum is just a circle around a point?

Mr. Yorage

Not quite. A Stratum is dynamic; it represents a region around a given planned development, and thus is technically different every time. But they often follow similar definitional patterns. For example, if there were a project being planned to expand Boston Latin School, our Strata might look like:

Ibn

So anyone in the country can vote on what happens here at Boston Latin?

Technically yes, but most don’t. Not everyone votes in every poll, but it’s important that anyone can.

But why should someone in San Francisco get to have any say on what happens here in Boston?

Well, maybe they want to move here?

But they don’t live here yet!

Mr. Yorage

Okay everyone, calm down. Janet, remember to use your indoor voice. You’re actually wrestling with a very reasonable and very difficult question. Whose opinion is valid on any given development? Is it the owners of the land? Them and the neighbors? People in the city? Just the city government? People who might want to move to the city? People who might want to live in a new development? People who want to move to the country?

It’s a really tough question, and one where the answer tends to vary across regions. Polis began as an experiment in distributed, anonymous blockchain voting. But because it’s not government-sponsored and therefore inherently non-binding, how it was used became open to a lot of natural experimentation.

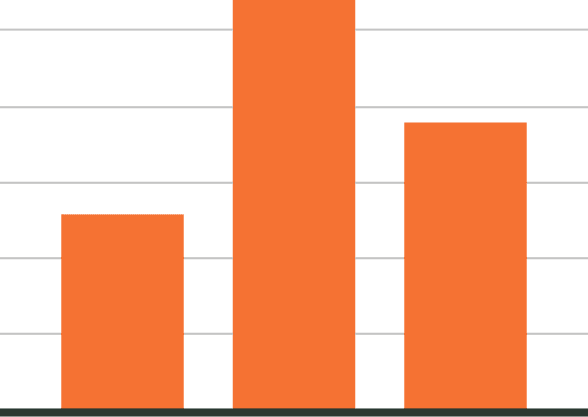

By convention, there are seven Strata regions created around each proposed project in a city, and voting is hosted on a secure, anonymous blockchain. The relative votes for and against in each Stratum are shown for each project. But then it gets more complicated! What does a city council do with that information? Those polling panels each represent a Stratum, a region of residents, whose perspective on a development can now be considered by the city council, along with the city bureaucrats and the voices of those able to attend the city meetings.

Over the last 50 years, each city has adopted its own mechanism of leveraging these polling panels. Some chose to ignore them entirely and continue with the previous limited-involvement decision-making systems. Some counted votes only within a certain distance, or adopted their own weighting system to value nearby votes higher than far away votes but still give everyone a say. The publicly validated nature of the blockchain gave credence to the votes, and more and more councils chose to utilize them, sometimes only as polls, but often as binding votes to drive their decisions.

This form of local development governance and distributed ownership is common nowadays, but was novel back when realcoins were first being introduced in the 2020s. Some scholars call the past few decades during which Groma has been dominant in urban areas the Era of Decoupled Housing, because urban property owners rarely live in spaces they fully own, but do nonetheless own more real estate wealth on average than in prior centuries. The resulting workforce mobility, interest in the future of the region as a whole instead of an individual property, and Polis have been broadly credited with a more efficient and equitable utilization and distribution of real estate than in the prior century.

4.1 Other Realcoins

Mr. Yorage

Okay, I see we’re running up on time here. I’m going to start to wrap this up and ask you to read the remaining sections of this chapter on your own.

While Groma is the largest of the realcoins today, it’s far from the only one. For the rest of class, you’ll be working in groups to investigate the history and effects of each of the other major realcoins in preparation for your homework tonight. You should see your groupmates' names on your SophOS.

Explore SophOS

- GigaJoule

As the spread of the Internet of Things enabled everyday consumers to track and modulate their energy consumption more precisely, people became increasingly aware of energy’s importance as an input in nearly every aspect of their lives.

With high inflation making dollars a much less reliable reference point for expressing the cost of various items, some people began to use gigajoules — the unit of energy equal to roughly one third of the average American home’s monthly energy consumption — as the go-to descriptor for expressing how much things cost.

Seizing on the inherent conceptual value presented by this, an enterprising startup inked contracts with the energy majors, spun up a blockchain, and began selling tokens that were exchangeable for exactly one gigajoule of energy at prevailing market rates.

- MooreCoin

By 2030, the average American between the ages of 18 and 85 spent 14 hours each week in virtual reality simulations. Many of these simulations were sufficiently demanding of computer processing power that users were charged on a per-minute basis. To facilitate payments, the leading VR distribution platform began to issue in-game tokens known as MooreCoins.

These tokens entitled users to a number of FLOPS defined based on the expected trajectory of Moore’s Law. Soon, MooreCoins and similarly situated competitors were widely used for computing tasks both in and outside of games.

- Asclepius

In the late 2020s, a number of large healthcare providers began to sell tokenized derivatives that derived their value from the providers’ combined operating profits. Healthcare consumers who wanted to safeguard their finances against future increases in the cost of healthcare could buy these tokens, which were branded as Asclepius after the Greek god of medicine, effectively foregoing immediate consumption or other investment opportunities to guarantee their ability to afford routine medical care at participating providers in the future.

This investment drove rapid acceleration in healthcare services, creating the core services that became part of what we now call the longevity industry, pushing human lifespan out further and further.

Want to get updates on Groma? Send a note to hello@groma.com to be added to our Newsletter!